12 min to read

Hippo recently announced that it sold a majority stake in First Connect for what appears to be a valuation of about 6 x revenue. I’m basing that on the $60M price and comment that November plus December revenues were expected to be between $1.5M and $1.8M (~$10M annualized). The article also noted that the sale would have a negligible impact on Hippo’s losses, meaning that First Connect doesn’t generate a profit.

I have an opinion on this topic, having evaluated several networks and Insurtech’s and having represented a few through sales. This is the lengthiest article that I’ve written so grab a drink and get comfortable while I step up onto the soap box.

We see insurance firms being pitched as Insurtechs frequently nowadays. The motivation to be labeled an “Insurtech” is the higher perceived market value of tech businesses over traditional insurance businesses. As one client said to me some years ago, “I’m told we can get 20 x EBITDA if we position our agency as an Insurtech!”

What really makes a tech company worth more than a traditional insurance firm?

Investors want a return on their money that is proportional to the investment risk. For an investor to pay 20+ x EBITDA, which is an extreme multiple for any company, necessitates that either the risk is almost non-existent (20 x EBITDA = 5% ROI, similar to a Treasury Bill) OR that there is high confidence that the value will grow significantly in the future (e.g., so that the 20 x eventually becomes 10 x).

For tech companies, the driver for extraordinary multiples is always the prospect of value growth. Think of Amazon, Netflix, Apple, and Tesla – their earnings multiples were off the charts at times because the market was confident in their ability to grow revenue and earnings significantly in the future. One fundamental difference between the aforementioned tech companies and Insurtechs is that the former created a market (blue ocean) while the latter is attempting to capture market share from an entrenched, competitive marketplace (red ocean). Tech companies sell tech products too; whereas most Insurtech’s are leveraging technology to sell an intangible product.

Years ago, we evaluated an Insurtech that was just under $10M in revenue. The company was being pitched to a client for acquisition. It had double digit revenue growth but was hemorrhaging cash with net losses piling up to well over $50M. Despite the massive losses, the sellers’ representatives were arguing that expenses could be gutted to generate an EBITDA margin over 75%.

We received a data dump for due diligence and went to work analyzing the business. In the end, my conclusion was that the business model was flawed, and business would struggle to achieve profitability (or run-off rapidly if expenses were cut dramatically post-acquisition, per the advisor’s proposal). My advice to the client was to pass on the deal.

The reason? Customer retention was too low and costs, including those to acquire new customers, were way too high. The company was spending 70-80% of its total revenue on sales & marketing alone and only generating 10-15% annual growth.

The Insurtech company, which no longer exists, checked the boxes:

They failed in two key areas: (1) not understanding the nature of the customer they were targeting and (2) not having a proven profitability model. On the former point, the company targeted online shoppers of insurance, who tend to be price-sensitive and churn (e.g. retention of 55-70%). On the later point, the company, backed by a VC firm, focused on top-line growth as if building a SAAS and ignored costs.

The pitch deck looked great. The financial performance was a nightmare.

Value to investors is derived from cash flow and equity growth. Since most Insurtech’s are not selling tech products, then the value of the tech is in leveraging it for growth and efficiency (i.e. equity growth). This is where the rubber meets the road. I don’t care if you are an agency or a carrier. How is the tech driving equity growth?

Let me focus on the capital backed Insurtech’s, as this is the most visible group.

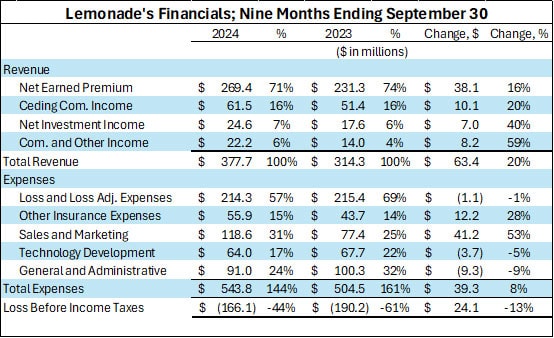

I mentioned the Insurtech we evaluated that was shy of $10M in revenue after burning well over $50M in cash. Let’s look at one Insurtech that has taken the stage, Lemonade[i], which has been described as “revolutionizing the insurance industry.” Here is a snapshot of its financials for the nine months ending September 30, 2024, compared to the prior calendar year.

This is a beautiful picture of what I’m talking about.

The point that I am trying to hammer home is that we’ve been listening to hype about Insurtech for nearly a decade now, but where is the real disruption? Global Insurtech investments passed $1.38 billion in Q3 alone.[v] Investors have plowed over $30 billion dollars into the space.[vi] Where are the big successes? Which Insurtechs have demonstrated an ability to grow profitably?

Going back to First Connect, kudos to Hippo for selling the platform for what I think was around 6 x revenue. I have not seen First Connect’s financials or book of business, so I can only make a surface-level assessment based on what is on its website and what I know about other networks. My guess is that its target demographic is smaller agencies that need a market for lines of business that those agencies don’t write frequently (e.g., cyber, small BOPs, manufactured homes, recreational vehicles, etc.).

The platform lacks relationships with key carriers that dominate in different regions of the country, like Travelers, Safeco, Liberty Mutual, Progressive, and Mercury. Therefore, First Connect will need to sign up a high volume of agencies, likely in the thousands, which will be tough to accomplish since over half of agencies are already a member of a network.[vii] Supporting a high volume of low production members adds significantly to administrative costs vs networks that work with fewer but larger agencies too. Outside of market access, most agencies join networks to become part of a club to share best practices and build relationships with other principals. Tech can’t replicate relationships, and that is an ongoing struggle for the space.

My intent with this article wasn’t to play the role of Statler & Waldorf and just poke fun from the balcony. It was to draw attention to two key points that I believe are being overlooked in the mad rush to “revolutionize the insurance industry.”

I’ll end by admitting that there is a lot I don’t understand about the Insurtech space. I’ve been privy to some behind-the-scenes data, and we’ve seen some big publicly announced failures in the Insurtech world (like WTW taking a ~$2 billion write off after the sale of the digital platform Tranzact).[viii]

I don’t understand why Lemonade, Root, and Hippo have $3.28 billion, $1.28 billion, and $648 million enterprise values, respectively, though when each one has been burning cash like trash in a homeless camp. I don’t understand why VC investors would plug $60M behind an insurance business that has $10M in revenue with negative cash flow and an unproven profit model. At some point these businesses need to make a profit, and one that supports the massive investments. I think that will be very challenging for some of them.

Time will tell the story of which Insurtechs survive. It will be interesting to look back and see exactly what ROI investors collectively obtained on Insurtech investments. As I joked on LinkedIn two years ago, R.I.P. to the revenue multiple and long live the ROI!

Posted by: Michael Mensch, Founder and CEO

Direct: (321) 255-1309

[i] https://investor.lemonade.com/financials/sec-filings/default.aspx

[ii] https://finance.yahoo.com/news/lemonade-inc-lmnd-bull-case-194504843.html?.tsrc=rss

[iii] https://www.linkedin.com/pulse/synthetic-bults-matteo-carbone/

[iv] https://discover.jdpa.com/hubfs/Files/Industry%20Campaigns/Insurance/2023USINSLISTQ1Report04202023.pdf

[v] https://www.insurancebusinessmag.com/us/news/reinsurance/ai-and-megarounds-drive-recordhigh-insurtech-funding–gallagher-re-513508.aspx

[vi] https://www.carriermanagement.com/features/2024/11/14/268559.htm

[vii] https://www.networksalliance.com/networks-study-summary/

[viii] https://www.insurancejournal.com/news/national/2024/10/01/795187.htm

We deliver superior results through our industry expertise, transaction expertise, and professional network.

Contact us